A typical nuanced view of the problem…

My father was in the private pension business before he died, and the idiocy of how Social Security was set up drove him to distraction. I’m pretty sure he voted for Ross Perot in 1992 because Perot argued that it made no sense not to means test the program. I’m tempted to take a copy of Robert J. Samuelson’s op-ed last week to Arlington National Cemetery and leave it on his gravestone.

Samuelson is reliably one of the most rational, thoughtful and probing of all the op-ed columnists. Last week he wrote about how the life-expectancy gap between the wealthier segments of U.S. society and the poorer ones made Social Security as it is currently constituted a significant contributor to the income gap that progressives desperately want to make a key issue in the 2016 election, because dividing the nation by class (and race, ethnicity, religion and gender) is a big part of their playbook.

“The figures come from a new report by the National Academies of Sciences, Engineering and Medicine, which estimated life expectancies for workers born in 1930 (now 85) and 1960 (now 55) at age 50. The findings are stark. For the richest fifth of men, there was a 7.1-year increase in life expectancy, from 81.7 for those born in 1930 to 88.8 years for those born in 1960. Meanwhile, for the poorest fifth of men, life expectancy fell slightly, from 76.6 years for those born in 1930 to 76.1 for those born in 1960. The changes for the remaining men also parallel income: For the second richest fifth, the increase was 8 years to 87.8 years; for the third richest, 5.3 years to 83.4 years; and for the fourth richest, 1.1 years to 78.3 years.”

Nobody should be surprised that wealth equals health. It is difficult to pinpoint why the gap is so large, but should we have to? It seems intuitively obvious. Many disadvantages–race, upbringing, family stability, good roles models, education, character, intelligence, opportunities, culture, neighborhoods—that undermine quality of life simultaneously or in combination with each other handicap earning ability and health before we even get to the question of medical care.

Samuelson goes on…

“Whatever the causes, the gaps in life expectancies dramatically affect federal spending on the elderly. Although Social Security and many programs for the aged were designed to favor the poor, the longer life expectancies of the middle and upper-middle classes offset this bias. Because richer male workers collect payments for more years than the poor, their lifetime benefits are much larger.The study estimated the present value of four federal programs for typical recipients (Social Security, Medicare, Medicaid and Supplemental Security Income). For the top fifth in income for men, lifetime benefits totaled $522,000, a third more than the $391,000 for the poorest fifth….We are spending the most money for the longest periods to protect people who need the least protection, because they have more private savings and pension benefits than do the poor…Does this make sense for us as a society? To me, the answer is: No.”

Samuelson reasonably concludes that Social Security needs to be fixed, both to make sure it stays viable, but also to more fairly distribute benefits:

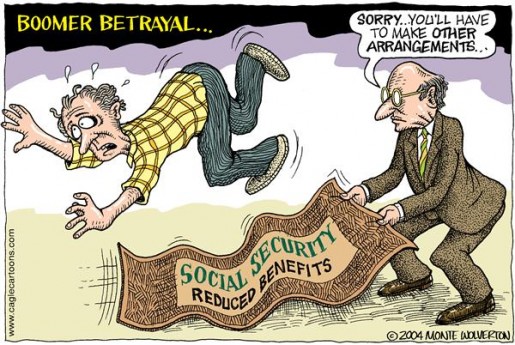

“Social Security should be a safety net, not a gravy train. As the number of retirees soars, so does the cost of paying their benefits. It’s squeezing other federal programs, creating pressures for higher taxes and sustaining long-term budget deficits. We are penalizing the future to pay for the past. We need (as I’ve often written) a fairer distribution of generational burdens. Eligibility ages for Social Security and Medicare should gradually increase to reflect longer life expectancies for most Americans. Benefits should be slowly curbed for those near the top.”

Or not so slowly. With the coming boom in seniors, either somebody’s benefits will have to be reduced or an increasingly small group of working young will find themselves paying more—that they need themselves to get their own lives off to promising starts—to support a hoard of self-righteous geezers who have retired to Boca Raton unless another administration, or three, decides to pretend the problem doesn’t exist and just adds more to the national debt. Social Security should be thought of as insurance: we pay for it during our working years as a hedge against failure or disaster. If we do not have other resources like accumulated wealth, investments, savings or pensions in our “Golden Years,” we still won’t be forced to eat from cans of Fancy Feast. If we don’t need it, then the money goes to someone who does.

The words for wealthy seniors who make the argument that no adjustment to their Social Security benefits is fair because “it’s a commitment” are selfish and greedy, as well as deluded and irresponsible. Somebody has to give up something, or Social Security goes bust. I recently heard that well-known impoverished pundit Sean Hannity make the commitment argument regarding his own future SS checks. Currently benefits usually exceed significantly what the beneficiaries put into the system. Okay, Sean, if a retiree is rolling in dough, give him back the amount he put in—with interest, I know you’ll insist on that— and make him wear a scarlet G on his chest evermore. I could support that.

Samuelson’s last word on the topic seems prescient.

“What looms is the status quo on steroids. Politics makes policy backward-looking. Programs for the elderly overwhelmingly benefit the middle and upper-middle classes but are defended by appeals for the poor. Some call this “progressive”; others might say cynical.”

Dad called it “idiotic.”

Welcome to Ethics Alarms Square Gardens to see the Main Event! In the red corner we have….

This should be good.

The system was set up as a pyramid, with a broad base of working young supporting a very few who made it to “retirement age.” When baby boom gave way to baby bust, the pyramid began to invert. Now, with the boomers reaching retirement in higher still numbers and there just being fewer and fewer new workers entering the force every year (partly because there are fewer jobs for them to enter) it’s completely upside down. Yet, those younger folks are now being told they will have to work longer and longer to get the same benefits…if there are any benefits by the time they get there. I’m fortunate enough that I got into the NJ pension system before Christie gutted it, and between SS, if I get there, and that I should be able to survive, but even that’s now up for question. I can see why a change would be resisted, I put 10 years in public service in, when arguably I might have done better in private practice ,with the understanding I would get a certain amount of benefits guaranteed. I don’t get those years back and I don’t get another opportunity to try my luck somewhere else if the state says “you know those benefits you were promised? We can’t keep the promise. I’m sure you can make other arrangements.”

In the end I think this is all academic, though. I think Ann Landers said it best when responding to a letter writer who expressed fear of elderly drivers and suggested that everyone over 65 get a mandatory annual eye test in order to keep their license. I don’t remember word for word her response was, but I can paraphrase it as “What you suggest makes a great deal of sense and is based on sound logic. However, the senior lobby has a lot of money and a lot of clout, and as such, it can never happen.” The fact is that those “geezers,” from the retired industrialist playing golf in Boca Raton who banks his SS checks he doesn’t need to survive so he can leave a tidy sum for his grandkids to go to college on to the silver-haired widow still living in the house she raised her kids in who takes part of her survivor check to go out to dinner once a week just to get out of the place, all have one thing in common: the belief that they worked, they paid their dues, they won the game by surviving, and now they get to enjoy the last years of their life free of the daily grind of work, and have others carry them as they carried those before. Any threat to that is going to be met with a powerful wave of contributions and political activity.

Wait a minute, are you sort of saying that Social Security is a kind of arrangement where new-comers pay in so older members get paid off and that those new comers need to wait for more new comers to pay in before they see returns?

I wonder if that kind of structure has been dealt with court rooms before?

Can someone say, “Ponzi”?

jvb

Of course it is. There’s no bucket of money funds go into from your check each pay period. It all goes right out the door to some retiree.

I like the idea of social security — but not the way it is structured now. I do think money should be taken out of our paychecks because it forces us to save. Let’s face it, most Americans are stupid when it comes to money management — really stupid. And that money should go into interest bearing accounts — but the government should not be able to borrow against it, ever. So, social security should be treated as a mandatory, untouchable 401(k).

Whether you are rich or poor, you get out the money that you put in. If the poor need additional money to meet basic survival, that should come from a separate fund — Medicaid Plus or something like that. If a person dies before his benefits have been tapped out, the same checks keep going to that person’s survivor until depleted. (I know that there is a survivor benefit right now, but it’s not the full amount and the percentage depends on age of survivor and some other factors.)

It will be interesting to see how this plays out. My generation is dealing with a lot more debt than our parents’ generation. Pensions are non-existent and I know many friends (who would otherwise be classified as wealthy) who are still paying student loan obligations well into their forties, some believe they will die with student loan debt. Retirement is a scary prospect.

If there is a pool of money anywhere that is administered by the federal government, no matter how it gets set up, a majority of elected officials will not be able to keep their hands off of it. The government is ten times more stupid with other people’s money as anyone is with their own.

The way it is, you tap out what you put in very quickly. In NJ, when I retire, I will get back every penny I put into PERS in a year, and after that, the taxpayers keep paying me. I’m still paying student loans from law school and expect to be for a while, although I did pay two of them off. A low starting salary (with promises of raises and bonuses that never materialized and were never intended to) meant there wasn’t much ability to knock a lot of it off out of the gate, and a later split in another firm I worked for left me in a pretty bad way (you know you’re in trouble when the partner calls you into his office and asks “what’s the absolute minimum you need to meet your monthly bills?” then cuts you down from there). Retirement is at least a possibility, I think I am likely to get a fairly substantial inheritance and I did vest in a pension, but still, it is a nerve-wracking thought.

Your assumption of taking out faster than it goes in doesn’t apply to those at the higher end.

I max out this month. I’m paying $880 a month for 10 months for a total of $8887 in SS taxes for the year. That’s not counting my employers $8887 they’re paying too. My projected retirement payouts are $1400 a month – for a total of $16,800 a year. I’ve got 25 years to “full” retirement age. Unless I live way past my expected lifetime, I’m not getting back out what I put in.

This depends on wether you feel social security is a retirement program or a welfare program. If it is a retirement program, then your proposal is preposterously unfair. Although the top fifth are getting 50% more money lifetime than the bottom fifth, they put in vastly more. My father paid in about $250,000 to SS in his lifetime. My wife’s grandmother put in nothing. His monthly benefit is 2.5x hers. Is that really unfair? If he receives 50% more than she does in lifetime benefits, is that really unfair?

Now, if you want to just say this is a welfare program and it has nothing to do with retirement, that’s different. If you want to means test it and punish people for saving for retirement, I guess that makes progressive sense. What you will end up with is even more people refusing to put money in IRA’s and 401k’s because it will reduce their Social Security payout. Remember, this is the payout from a program that consumes 15% of their income for their entire working life.

Remember government means tests are geared to help the irresponsible. Look at student financial aid. If your parents make $500,000/year and have 3 vacation homes, 2 boats, and 10 cars, you qualify fro grants because you have $600,000 in debt. If you make $40,000, but have a small house and buy cars with cash, you don’t qualify because you family has no debt. Do you really want a means test like that for Social Security? Don’t pretend it won’t be like that because that is how all government means tests are.

1. If we hold to the original purpose of SS, obviously its a social welfare program. It was never intended as a retirement program, and as a retirement program, it’s inefficient as hell.

2. Settle on the use of “fair.” Samuelson is using the Left’s fair, and pointing out that it doesn’t apply. Personally, I see nothing unfair about income inequality at all.

3. I do see things wrong with hypocritical, bankrupt government Ponzi schemes that won’t address their own bad math and demographics.

4. You’re arguing that a reasonable fix isn’t reasonable because the government will botch it. That’s not a fair argument against the fix, just against the agent.

My argument is that if you argue for a means test, you should accept the reality of what a means test would be. The only means tests the government has are the one I described, and that would make the retirement situation worse.

Title IX may have been a reasonable fix, but it has set up rape tribunals on college campuses across this country. Is an argument against Title IX invalid because it was a reasonable fix that the government botched? When someone has proven incapable of doing a job over and over again, giving them the job again becomes irresponsible. It may be an argument against the agent, but you are the one who suggested using that agent.

“My argument is that if you argue for a means test, you should accept the reality of what a means test would be.”

That is assuming that what has been done badly in the past must be done badly in the future. It’s a rationalization: 1A. Ethics Surrender, or “We can’t stop it.” with a bit of 41. The Evasive Tautology, or “It is what it is.” It means that a bad program must be continued in flawed form forever. That’s not just unethical—it’s wrong not to fix a program that will lead to disaster— it’s crazy.

But one definition of insanity is doing the same thing over and over again and expecting a different result.

My blog hated this comment so much I had to approve it, apparently. That definition of insanity is a facile rationalization for giving up, especially in politics and government, don’t you think?

Jack,

Your proposal will complete the lie that is the social security system.

They took people’s money away and they could only do it because they promised that it was money set aside for them later.

(The anger this caused people is the very reason people want to take every penny out of the system that they are allowed.)

Then, some years later, the Supreme Court said, “no, you don’t have ANY property right in the money they took from you.” (That is a paraphrase.)

Now, they want to means test it. With that, it will become what they denied it was all along: welfare and wealth distribution.

I hate Social Security, but would never take it away from those who have reached or are about to reach retirement. But, I know it won’t be there for me and I would be fine scrapping it for everyone under 50 (for example).

But, the saving grace is that, at least, a recipient can say, “I paid in and am just getting that money back.” It not welfare. Take that rationale away, and it is just another welfare slush fund.

And, we will be at the bottom of the slope.

-Jut

How can being up front about how the money will be distributed be a lie?

But they aren’t being upfront about it. They have taken my money for decades and they never said they would means test it. Now they are going to means test it? Sounds like a bait and switch to me!

It’s only a bait and switch if that was the plan all along. If changed circumstances require changes, they require changes. Kim Davis can claim a bait and switch on that basis.

The plan all along? What do you think progressivism is, if it is not a death by a thousand cuts. People who hated the deductions fight for every penny of payment they can get. It was a lie at the start. We are only now seeing the result they planned all along.

Oh, but maybe you thought they believed they could win the War on Poverty too.

-Jut

Even I’m not that cynical. The original Social Security made sense because of shorter life spans and demographics. This is a perfect example of Hanlon’s Razor—not malice, just stupidity.

Not even stupidity, just incomplete information and changing circumstances. I guess we’d be better off if Grace had overseen it (their commercial tagline was “Grace is One Step Ahead of a Changing World”).

The Roots of the Social Security Myth , a revealing article by John Attarian, may shed some light on this issue. It illustrates to what depths Social Security proponents and the media are willing to sink in their effort to maintain the retirement fund myth.